Europe Green Methanol Market to Reach USD 1.12 Billion by 2032, Growing at 9.6% CAGR

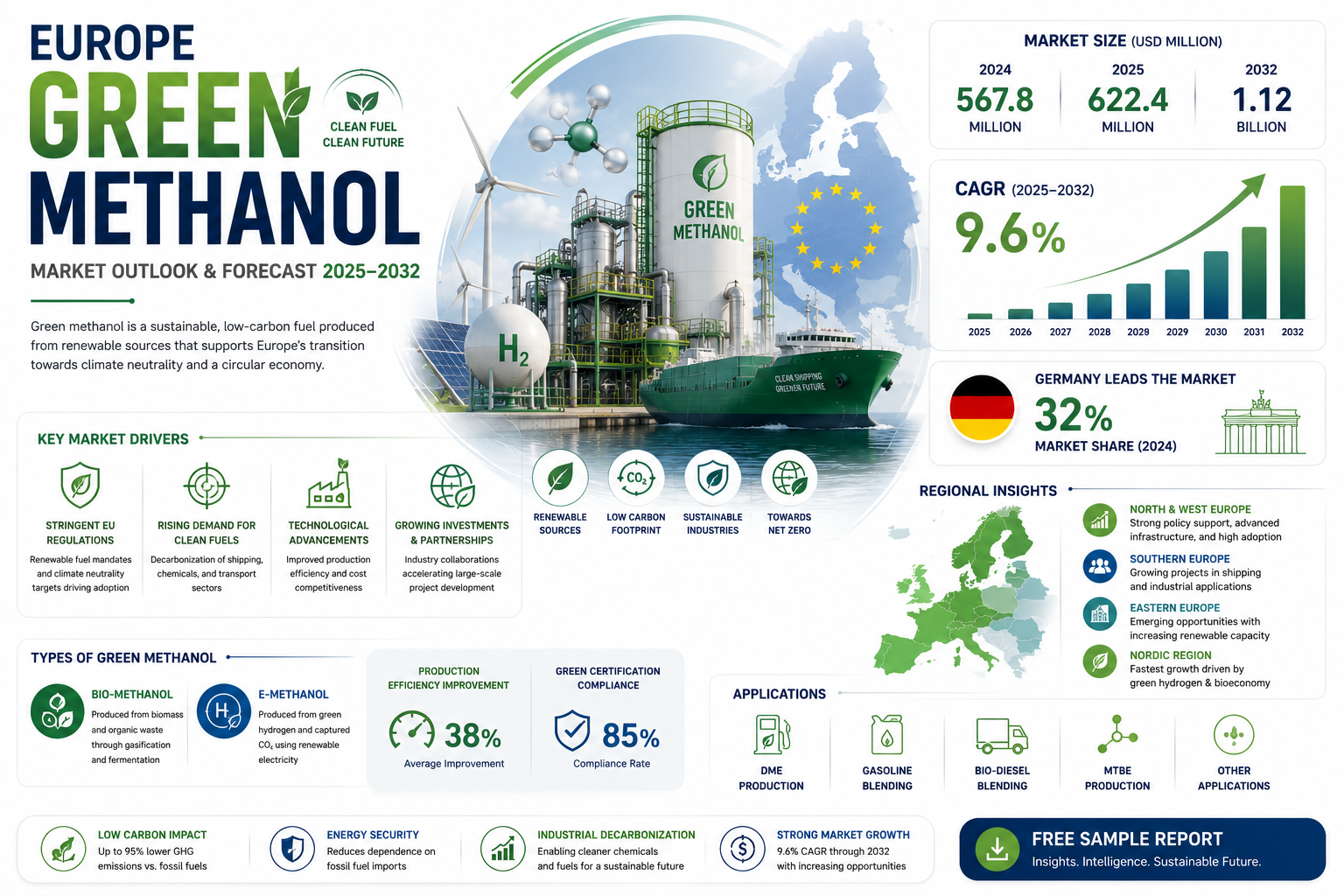

The Europe Green Methanol market size was valued at USD 567.8 million in 2024. The market is projected to grow from USD 622.4 million in 2025 to USD 1.12 billion by 2032, exhibiting a CAGR of 9.6% during the forecast period.

Green methanol is an environmentally sustainable fuel produced from renewable sources such as biomass, captured carbon dioxide, or green hydrogen. This low-carbon alternative plays a crucial role in decarbonizing industries including chemicals, transportation, and energy, aligning with Europe's ambitious climate neutrality goals. The fuel is categorized into bio-methanol (from biomass) and e-methanol (from renewable electricity and captured CO2).

Market growth is driven by stringent EU regulations mandating renewable fuel adoption, with Germany leading at 32% market share. The chemical sector accounts for 45% of current consumption, while production efficiency improvements (averaging 38%) and adherence to green certification standards (85% compliance) further bolster adoption. Recent collaborations, like Siemens Energy's 2024 partnership with BASF to scale e-methanol production using wind power, demonstrate industry momentum towards sustainable solutions.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/285061/europe-regional-green-methanol-forecast-supply-dem-analysis-competitive-market

Market Overview & Regional Analysis

Germany occupies the forefront of Europe's green methanol landscape, consolidating its position through a dense concentration of biorefinery projects, extensive infrastructure, and supportive public policies. The country's well-established chemical network and its commitment to integrate renewable feedstocks into the energy mix create a synergistic environment that attracts large capital flows. Meanwhile, the United Kingdom, Netherlands, and France provide complementary platforms owing to their advanced logistics corridors and favorable regulatory frameworks. Globally, German initiatives serve as a benchmark, influencing policy design elsewhere in the region. The cumulative effect of prolonged investment, forward-looking technology adoption, and coherent market signals has positioned the German market as the most mature and scalable within Europe.

Robust biorefinery cluster driving supply capacity, allyship between academic research and industry innovation, advanced logistics easing regional distribution, co-financing mechanisms spurring project viability, and dynamic policy mix incentive for renewable feedstock sources.

The Nordic corridor, particularly Sweden and Finland, is emerging as the fastest-growing segment. Rising energy security concerns and the drive to replace imported hydrocarbons with domestic renewable solutions have accelerated the deployment of green methanol plants. Capital projects are being fast-tracked through state-backed climate funds, which buffer financial risks and build industry confidence. Simultaneously, the Soviet-Black Sea region, with its legacy of large chemical hubs, presents an opportunity given forthcoming decarbonization mandates. The interplay of public subsidies, market readiness, and technological importation enhances the pace of transition, leading to steeper growth trajectories relative to more established Western markets.

Climate-aligned government financing pipelines, early-adopter status in hydrogen and bio-feedstock integration, strategic partnerships between national grid operators and green producers, consistent policy clarity reducing regulatory friction, and high visibility of industry associations driving standardization.

Expanded biorefinery footprints act as localized renewable hubs, shifting demand southwards to regions closer to feedstock sources. The construction of dedicated pipelines and bulk storage units has created a realistic long-term supply chain, mitigating volatility that typically deters investment. Coupled with EU-level projects that enhance cross-border connectivity, these infrastructural upgrades lower logistics costs and foster market integration. The resulting network effect encourages new entrants in adjacent economies, thereby redistributing demand from traditional single-source suppliers to a more diversified, regionalized market structure. Over time, the improved physical logistics backbone has helped standardize production processes and pave the way for a coherent European green methanol corridor.

Pipelines reinforcing cross-border supply reliability, storage facilities enhancing regional resilience, reduced transportation costs boosting production incentives, integration of renewable feedstock supply chains, and supportive regulatory scores increasing project feasibility.

France, Belgium, and the United Kingdom are attracting significant investor attention. Their rigorous environmental standards, coupled with generous fiscal incentives such as tax credits and grants, provide a compelling risk-return profile. Strong industrial clusters, already proficient in chemical manufacturing, offer asset synergies that minimize learning curves. Additionally, these nations are cautious about aligning with EU emissions targets, pushing them to adopt renewable solutions early. Engaging local governments facilitate streamlined permitting processes, accessing fast-track approvals that substantially cut project timelines. Finally, the presence of research institutes and innovation hubs ensures access to cutting-edge technology, thereby reducing technology risk for foreign investors.

Favorable fiscal frameworks diminishing entry barriers, advanced industrial legacy reducing operational risk, streamlined regulatory pathways expediting approvals, robust R&D ecosystems lower technology risk, and strategic positioning within EU decarbonization strategies.

Key Market Drivers and Opportunities

The European Union's Green Deal and the Sustainable Finance taxonomy have created a robust regulatory framework that incentivizes low-carbon fuels. Because member states are aligning national energy plans with these targets, investors are channeling capital into green methanol production facilities. Policy certainty therefore acts as a catalyst for market expansion.

Maritime operators are under pressure to meet IMO's 2025 carbon intensity reduction goals, while airlines are exploring sustainable aviation fuels to comply with EU Emissions Trading System mandates. While traditional bunker fuels remain dominant, the shift toward carbon-neutral alternatives is accelerating, making green methanol an attractive option for both sectors.

Green methanol provides a carbon-neutral fuel pathway that can be blended directly into existing diesel infrastructure, reducing the need for costly retrofits. Furthermore, the versatility of green methanol-as a fuel, a chemical feedstock, and an energy storage medium-creates cross-sector synergies that reinforce demand. Stakeholder collaboration across energy, transport, and finance is strengthening the market's growth trajectory.

European producers can leverage the region's technological edge to supply green methanol to fast-growing markets in North Africa and the Middle East, where maritime traffic is high and renewable fuel mandates are being introduced. This export potential diversifies revenue streams and reduces reliance on domestic demand cycles.

Advancements in electrolyzer efficiency and modular carbon capture units are driving down production costs, making green methanol increasingly competitive. Companies that adopt these next-generation technologies early are positioned to capture a larger market share. Strategic partnerships between petrochemical firms and renewable energy providers are fostering integrated value chains, enabling seamless conversion of excess renewable electricity into methanol. Such collaborations enhance scalability and reinforce the sector's long-term viability.

Challenges & Restraints

Europe's current fuel distribution network was designed for conventional hydrocarbons, and retrofitting pipelines, storage tanks, and bunkering facilities to handle methanol poses technical and safety challenges. Because the adaptation process requires significant capital outlays, many operators delay investments. Additionally, the lack of standardized blending ratios and certification procedures hampers large-scale adoption, forcing producers to navigate fragmented regulatory landscapes across different jurisdictions.

Renewable hydrogen and captured CO₂, the primary feedstocks for green methanol, are still more expensive than fossil-derived counterparts. While economies of scale are expected to improve margins, the current cost differential limits price competitiveness against traditional fuels.

Securing a reliable supply of low-carbon hydrogen and sustainably sourced CO₂ is a critical bottleneck. Seasonal variations in renewable electricity generation affect hydrogen production capacity, while the capture of industrial CO₂ depends on the continued operation of emitters undergoing decarbonization. Price volatility of renewable electricity further exacerbates the issue, as it directly influences the cost structure of green methanol. Without stable feedstock pricing, project financing becomes riskier for investors. Regulatory uncertainties surrounding carbon accounting methodologies also create hesitation among potential adopters, who fear future compliance costs.

Market Segmentation by Type

● By-Product Sourced Bio-Methanol

● Waste Sourced Bio-Methanol

The European market increasingly favors waste-sourced bio-methanol due to its alignment with circular-economy principles and regulatory incentives for waste valorisation. Companies that can integrate municipal solid waste or agricultural residues into methanol production enjoy differentiated positioning, as this approach reduces reliance on virgin feedstocks and demonstrates tangible carbon-reduction narratives. By-product sourced methanol, while still relevant, is perceived as a secondary option, primarily used where industrial by-products are abundant and logistics allow seamless capture. The strategic emphasis on waste streams is driving innovation in pre-treatment technologies and partnerships with waste management firms, fostering a more resilient and environmentally credible supply base across Europe.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/285061/europe-regional-green-methanol-forecast-supply-dem-analysis-competitive-market

Market Segmentation by Application

● MTBE

● DME

● Gasoline Blending

● Bio-diesel

● Others

In Europe, the application of green methanol as a feedstock for dimethyl ether (DME) and as a gasoline blending component is gaining traction, driven by stringent renewable-fuel mandates and the desire to decarbonise transport fuels. DME, with its clean-combustion profile, is viewed as a strategic bridge toward zero-emission mobility, especially in regions pursuing hydrogen-compatible infrastructure. Simultaneously, methanol-enhanced gasoline offers immediate emissions benefits without overhauling existing refineries. The sector is also exploring niche uses such as MTBE replacement for octane enhancement, where policy incentives encourage low-carbon alternatives. These application pathways collectively shape demand patterns, encouraging manufacturers to tailor product specifications to meet diverse fuel-quality standards across the continent.

Market Segmentation and Key Players

● BASF SE (Germany)

● Siemens Energy (Germany)

● Preem AB (Sweden)

● Nordic Green (Denmark)

● Liquid Wind (Sweden)

● BioMCN (Netherlands)

● Proman (Netherlands)

● St1 (Finland)

Report Scope

This report presents a comprehensive analysis of the global and regional markets for Frequency-to-Current Signal Converters, covering the period from 2026 to 2034. It includes detailed insights into the current market status and outlook across various regions and countries, with specific focus on:

● Sales, sales volume, and revenue forecasts

● Detailed segmentation by type and application

The report features in-depth competitive intelligence including:

● Market share analysis of leading manufacturers

● Production capacity expansions

● Product portfolio assessments

● Strategic partnership evaluations

Our research methodology combines primary interviews with industry leaders and comprehensive data analysis of:

● Production facilities and their geographical distribution

● Raw material sourcing patterns

● End-user industry consumption trends

● Regulatory impact assessments

Get Full Report Here: https://www.24chemicalresearch.com/reports/285061/global-aluminum-plate-sheet-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

● Plant-level capacity tracking

● Real-time price monitoring

● Techno-economic feasibility studies

With a dedicated team of researchers possessing over a decade of experience, we focus on delivering actionable, timely, and high-quality reports to help clients achieve their strategic goals. Our mission is to be the most trusted resource for market insights in the chemical and materials industries.

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Follow us on LinkedIn: https://www.linkedin.com/company/24chemicalresearch